The Birthday Rule: How this looks from a Closed Block Perspective

Sixteen states have enacted birthday rules — provisions that allow Medicare Supplement policyholders to switch to an equal or lesser plan during a window around their birthday each year, without being subject to medical underwriting.

In analyzing CSG Actuarial’s open and closed block rate data feeds alongside experience data across all 50 states, comparing the size of the open and closed blocks in birthday rule states, how those blocks compare to non-birthday states.

1. Block Size in Birthday Rule States: A Large Pool of Potential Switchers

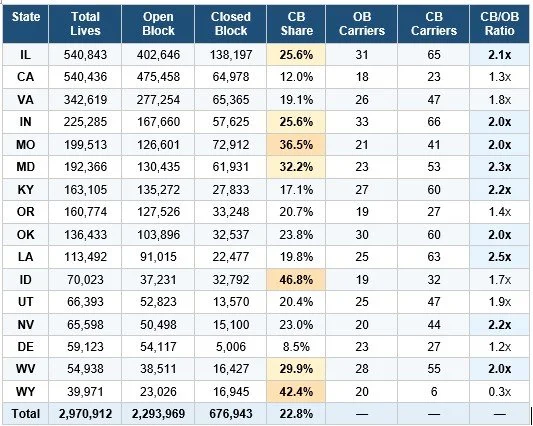

Nationally, the open block holds approximately 10.0 million Medicare Supplement lives, while the closed block holds 3.7 million — meaning roughly one in four policyholders is in a block that is no longer accepting new members. Across the 16 birthday rule states, closed block policyholders number at least 677,000 based on NAIC experience data, representing approximately 22.8% of all covered lives in those states. The state-by-state picture, however, varies considerably:

Data:: Plan G, Female, Age 75, Non-Tobacco rates shown unless noted.

The two largest birthday rule states — Illinois and California — together account for over 1.08 million lives. But their closed block dynamics differ sharply. In Illinois, more than 1 in 4 policyholders (25.6%) is in a closed block, with 65 distinct closed block carriers versus just 31 open block options — a 2.1x ratio. California, despite a similar total market size, shows a much smaller closed block share (12.0%) and a CB/OB carrier ratio of just 1.3x, suggesting a market that has consolidated more cleanly into open products over time.

The states with the highest closed block concentration tell a different story. Idaho leads at 46.8% — nearly half of all covered lives in the state are in closed blocks — followed by Wyoming (42.4%) and Missouri (36.5%). These are states where a large share of the current policyholder base entered products that have since closed, and where the accumulated pool of potential switchers is proportionally the largest.

Wyoming is a notable outlier on the carrier side: despite a 42.4% closed block share, it has only 6 closed block carriers compared to 20 open block options — a 0.3x ratio that is the inverse of nearly every other state. This unusual structure reflects Wyoming's small, community-rated market and drives the atypical pricing dynamic discussed in Section 3.

Louisiana presents the opposite extreme on carrier counts: 63 closed block carriers versus 25 open block options — a 2.5x ratio, the highest of any birthday rule state. Despite a modest 19.8% closed block share by lives, the sheer number of distinct closed products means policyholders are spread thinly across many aging pools, amplifying the risk of closed block spiral for individual carriers.

Why does the carrier ratio matter as much as the share? Each closed block represents an independent pricing unit. When a carrier closes a block, it can no longer offset deteriorating claims experience with younger, healthier new entrants. The more fragmented the closed block landscape — many small pools rather than a few large ones — the faster each pool ages, and the faster rates tend to escalate. States like Maryland (2.3x), Kentucky (2.2x), and Nevada (2.2x) combine high carrier ratios with meaningful closed block shares, creating conditions where rate pressure is most likely to accelerate.

In all of these states, the birthday rule is the only mechanism that gives policyholders a cost-free exit. Without it, they are effectively captive — locked into a closed pool whose rate trajectory is driven not by their own health, but by who has already left.

2. How Do Birthday Rule States Compare to Non-Birthday States?

The absence of birthday rules doesn't change the underlying economics: closed blocks in non-birthday states show nearly identical premium gaps relative to open block options (+17.6% vs. +16.1% at age 75).